For years, retail returns were treated as an unavoidable cost of doing business, an operational issue delegated to supply chain, store operations, or customer service. This framing is no longer holds. Omnichannel retail environments position returns as an unplanned return-related costs that directly threaten retail profitability and returns, undermine margin forecasts, and quietly erode enterprise value. These costs rarely appear cleanly on a P&L, yet they compound across revenue, logistics, labor, inventory, and fraud exposure.

For CFOs and senior finance leaders, the question is no longer whether returns matter financially. It’s whether the organization truly understands their full financial impact and has the controls in place to manage them. Returns fraud, return policy leakage, and reverse logistics inefficiencies are converging into an important financial risk frontier. One that traditional financial models often fail to capture.

Why Retail Profitability and Returns Are Now a CFO-Level Issue

Returns sit at the intersection of revenue recognition, inventory valuation, logistics expense, and fraud risk. When left unmanaged, they inject volatility into what should be predictable financial outcomes. Returns convert realized revenue into delayed, discounted, or unrecoverable inventory, while adding labor, transportation, and processing costs that do not scale efficiently. The impact is not linear. As return volumes grow, margins compress faster than sales expand. This is why retail profitability and returns have become inseparable and why returns are now a CFO-level issue, not just an operational one.

How Do Returns Affect Retail Margins?

At a surface level, returns reduce net revenue, but in reality, that is often the least damaging effect, and often the least damaging. Returns erode retail margins through multiple, compounding layers:

- Lost gross margin from refunded transactions

- Incremental labor and handling costs

- Transportation and reverse fulfillment expenses

- Inventory markdowns, write-offs, or obsolescence

- Fraud losses absorbed as “customer service”

Taken together, returns compress margins by turning realized revenue into assets that lose value over time while layering in costs that are difficult to forecast or recover. This is margin erosion disguised as customer convenience.

The Financial Impact of Returns Is Larger Than Reported

Most finance teams track return rates. Far fewer can quantify the true financial impact of returns. This is because return-related costs are fragmented:

- Transportation costs live in logistics

- Processing labor sits in operations

- Fraud losses are buried in write-offs

- Inventory devaluation surfaces later through markdowns

This fragmentation masks the real economic burden. Even modest increases in return volume can create outsized margin pressure once downstream effects are included. The gap between reported return expense and actual economic loss is where profitability quietly disappears.

Returns Fraud and Policy Abuse: Margin Erosion in Plain Sight

Returns fraud has evolved well beyond isolated bad actors. It includes wardrobing, bracketing, receipt fraud, item switching, and excessive “friendly fraud” behavior that passes through standard workflows undetected.

From a finance lens, the question is: How does return fraud impact profitability?

The answer lies in scale and invisibility. Fraudulent and abusive returns create persistent return policy leakage, value leaving the business without triggering traditional fraud controls. Individually, incidents appear immaterial. Collectively, they are massive.

According to Appriss Retail, fraudulent and abusive returns exceeded $100 billion in 2024 losses for U.S. retailers, much of it embedded within standard refund and write-off processes (Appriss Retail). Because these losses are framed as customer accommodation rather than financial risk, they often escape governance scrutiny, creating a material control gap for CFOs.

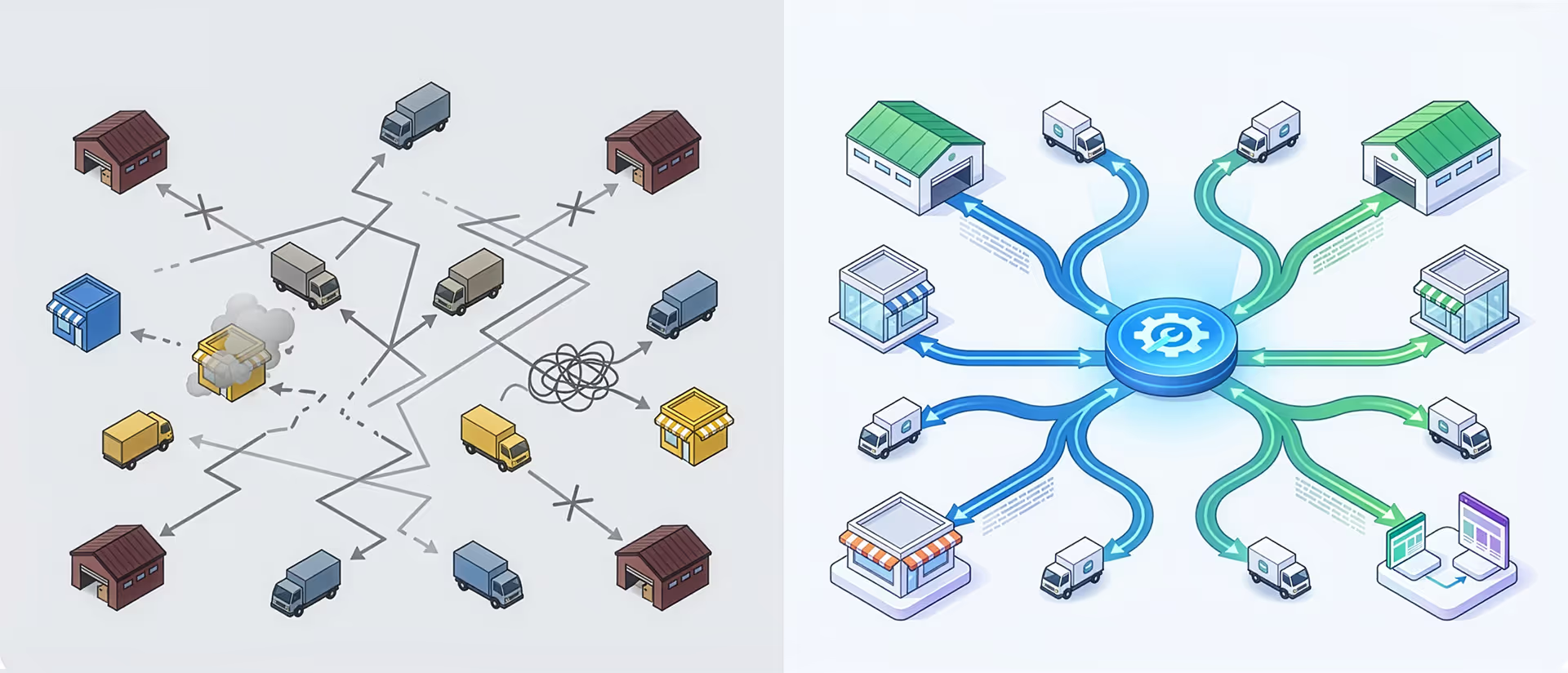

Reverse Logistics: The Hidden Cost Center

Reverse logistics has become one of the fastest-growing cost centers in retail, and one of the least optimized financially. When finance leaders ask, “What is the financial cost of reverse logistics?”, the answer is sobering. Industry research estimates reverse logistics activities account for nearly 1% of total U.S. GDP, reflecting the cumulative cost of return transportation, inspection, sorting, refurbishment, restocking, and disposal across the retail ecosystem (UPS Supply Chain Solutions, Reverse Logistics White Paper).

Reverse logistics includes:

- Transportation from customer to store or warehouse

- Inspection, sorting, and repackaging

- Refurbishment, liquidation, or disposal

- Systems and labor required to manage return flows

Without deliberate reverse logistics cost reduction, return volumes can grow faster than sales, creating the illusion of revenue growth while margins steadily deteriorate.

Reverse Logistics Cost Reduction Requires Financial, Not Just Operational, Control

Many retailers attempt to address reverse logistics through operational efficiency alone. Without financial oversight, these efforts rarely deliver sustained margin improvement.

True cost reduction requires understanding how return pathways, processing speed, and routing decisions translate into recoverable value or permanent loss. Without that visibility, reverse logistics becomes a cost sink rather than a controllable system.

Inventory Value Recovery: The Overlooked Profit Lever

Inventory value recovery is one of the most under utilized levers in returns management. Returned inventory is not binary. Its value exists on a spectrum shaped by speed, condition, routing decisions, and demand timing. As returned items sit idle, recoverable value decays rapidly.

From a CFO perspective, poor inventory value recovery represents trapped capital, assets already paid for but never fully monetized. Improving recovery rates often delivers margin gains equivalent to top-line growth, without acquiring a single new customer. Achieving that requires real-time visibility into item condition, routing decisions, and recovery outcomes, capabilities increasingly enabled through platforms like ReturnPro, which connect return activity directly to recovered margin and working capital performance.

Reduce Return Costs Without Damaging Customer Experience

A common concern among finance leaders is that efforts to reduce return costs will harm customer loyalty. In practice, the opposite is often true.

The most effective strategies move away from blanket policies toward precision:

- Differentiating legitimate customer behavior from high-risk activity

- Applying targeted return fraud prevention

- Routing inventory based on recoverable value, not convenience

Data-driven controls protect margins while maintaining trust. The goal is not restriction; it’s alignment between customer experience and financial reality.

How Can CFOs Better Model Return Costs?

When asked, “How can CFOs better model return costs?”, the answer is to treat returns as a variable financial system, not as a static percentage of sales.

Effective modeling requires:

- End-to-end cost attribution across logistics, labor, fraud, and inventory

- Scenario-based forecasting to understand margin sensitivity

- Behavioral segmentation to identify disproportionate cost drivers

- Inventory outcome tracking tied to recovery value and speed

When returns are modeled with the same rigor as pricing or demand, finance leaders gain leverage, not just insight.

Return Policy Leakage Is a Finance Problem

Return policies are often owned by merchandising or CX teams, but their financial consequences belong squarely to the CFO. Every exception, loophole, or unmanaged threshold creates return policy leakage, value exiting the business without strategic intent. In an environment of rising fulfillment costs and tightening margins, unmanaged leakage is no longer acceptable. Leading retailers now treat return policies as governed financial instruments, aligned to profitability targets and risk tolerance.

Final Thought: Returns Are the New Margin Battlefield

In a market with constrained pricing power, rising acquisition costs, and relentless pressure on capital efficiency, retailers can no longer afford blind spots in their financial models. Returns fraud, policy abuse, and reverse logistics inefficiencies represent one of the largest and least controlled sources of margin erosion in modern retail. They also represent one of the last meaningful opportunities for CFOs to unlock profitability without increasing demand or cutting growth investments.

This shift requires more than better reporting. It requires purpose-built financial infrastructure that gives leaders visibility into return-related costs, fraud exposure, inventory recovery, and policy leakage, so decisions are grounded in economic reality. This is why retailers are increasingly leveraging platforms like ReturnPro as a financial control layer, not only to manage returns operationally, but to quantify risk, model return costs, and protect margin across the enterprise.

As margin pressure intensifies and capital efficiency becomes a primary growth lever, returns are emerging as a strategic financial frontier. A frontier where CFOs can actively shape future profitability, risk exposure, and long-term performance.